It wasn't a tough prediction, but late Friday morning Noel Sheppard at NewsBusters noted the seemingly "metaphysical certitude the Obama-loving media will be falling over themselves in the next 48 hours to report the better than expected jobs numbers in June." Well, of course.

Noel also wondered how much attention the press would pay to less than desirable aspects of yesterday's jobs report from Uncle Sam's Bureau of Labor Statistics. The answer at the Associated Press, aka the Administration's Press, which carried at least eight reports relating to the news and its effects on the financial markets, was "hardly," as will be seen in excerpts after the jump. Additionally, the AP reversed its initial take that yesterday's non-change in the unemployment rate would keep the Federal Reserve's stimulus flowing, later deciding that the jobs report was so good that the Fed can let the tapering begin.

There was plenty to not cheer about in yesterday's jobs report, even after acknowledging that the total increase in seasonally adjusted payroll employment of 265,000, including combined upward revisions to April and May of 70,000 on top of the 195,000 added in June, was a pretty decent though arguably overstated number -- at least in the context of the past few years (but not compared to results seen in the mid-1980s, especially after adjustments for workforce size).

There was a steep single-month loss of 240,000 full-time jobs, which was accompanied by an even larger 360,000-person increase in part-time employment. The jobs added were disproportionately in low-paying fields with heavy part-time participation (e.g., 51,700 jobs added in "food services and drinking places"). There were also increased signs of low morale, including the the 322,000-person increase to 8.2 million in those who are part-timers for economic reasons, and a year-over-year increase of 206,000 (to 1 million) in the number of discouraged workers.

As to the markets' favorable reaction to yesterday's report (the Dow, S&P, and NASDAQ each advanced by 1 percent), those who believe that it was because the news was so good have conveniently forgotten that the markets have recently dropped at any hint that Ben Bernanke's Federal Reserve might "taper" its quantitative easing program, otherwise known as "hitting the 'enter' key to create money out of thin air." The first AP unbylined AP dispatch just 23 minutes after the BLS report was released gave away that more likely reason why stocks advanced in pre-market trading and remained up during the trading day:

FUTURES LEAP AFTER SURPRISINGLY STRONG JOBS REPORT

The unemployment rate remained at 7.6 percent, however, which leaves open the door for extended stimulus measures that have been undertaken by the U.S. Federal Reserve.

As long as the "stimulus" continues at its current rate, the stock market will probably stay artificially propped up. In other words, the news was sufficiently non-positive to instill confidence that the "stimulus" will continue.

An hour later, the tune changed in an unbylined blurb shortly after the markets opened:

STOCK MARKET RISES AFTER STRONG US JOBS REPORT

Robust hiring in the U.S. is boosting the stock market in early trading.

The next unbylined AP report followed in mere minutes, relaying the White House's spin and its predictable whining about "spending cuts":

WHITE HOUSE CALLS JOBS REPORT A SIGN OF RECOVERY

The White House says the June jobs report is good news that further confirms the economic recovery.

... The White House is battling Congress over how much to cut the federal budget, with Obama arguing that immediate spending cuts are hurting the recovery.

The next unbylined item could have been subtitled "Women, especially African-American women, hardest hit":

JUNE BRINGS MORE US JOBS TO MEN AND TEENAGERS

... for adult men, who make up a slight majority of the workforce, June was a time of improvement.

... Early-summer hiring wasn't quite as kind to adult women. Their unemployment rate rose to 6.8 percent, up from a four-year low of 6.5 percent. And unemployment for black women 20 and older shot up to 12 percent, from 11.2 percent in May.

The next unbylined report did a smiley-face routine on all the wonderful hospitality and retail jobs added without focusing at all on how these industries generally don't pay well and make heavy use of part-timers:

RETAIL AND SERVICE FIRMS DRIVE JUNE US HIRING

June's robust hiring was driven again by the U.S. service industry, signaling growing confidence in the American consumer.

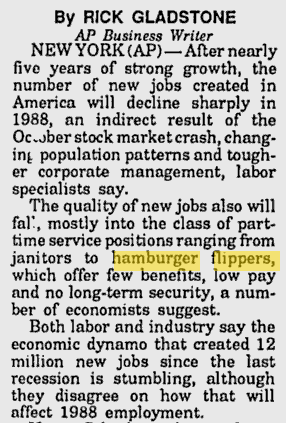

The hospitality industry, which includes restaurants, hotels, casinos and amusement parks, led all groups with 75,000 added jobs. More than two-thirds of those were at restaurants.

In the mid-1980s, these jobs were ridiculed as "hamburger flippers" by an AP reporter and others, which, as is still the case, offer "few benefits, low pay and no long-term security." There's no such ridicule now, even though the mix of jobs added in the 1980s was far more high-paying by the living standards of that era than we are seeing today.

A 1 p.m. report on the stock market by Christina Rexrode stuck with the "market is up because the jobs report is so great" meme:

STOCKS HOLD ONTO GAINS AFTER STRONG JOBS REPORT

The stock market is slightly higher after giving up early gains fueled by a strong jobs report.

An early afternoon report on the difference between the two surveys the BLS uses to compiles its statistics missed every opportunity to point to the negatives in yesterday's numbers, but it did make an interesting observation:

Unlike the payroll survey, the household survey captures farm workers, the self-employed and people who work for new companies. It also does a better job of capturing hiring by small businesses.

The difference between total employment in the household and establishment surveys has been narrowing, because the trends in the number of self-employed and in micro-business job creation have generally been down.

After the closing bell, the meme held, as another unbylined report led by telling readers that "The U.S. stock market is closing higher after a bumpy start, with investors encouraged by a big uptick in hiring." As noted earlier, the AP started the day by claiming that the markets were encouraged by the flat unemployment rate and the implication that Big Ben would keep the stimulus flowing.

At 5:35 p.m., the AP's Christopher Rugaber, with help from Martin Crutsinger, named "Worst Economics Writer" in America by Kevin Williamson at National Review, tried to have it both ways:

The government says that the U.S. economy added a stronger-than-expected 195,000 jobs last month. That helped investors shake off worries about the Federal Reserve scaling back its economic stimulus, which spooked markets early.

After his own wire service opened the festivities by saying that the flat unemployment rate was good news because Big Ben won't taper, Rugaber appears to have been trying to say that the numbers were so strong that investors aren't even worried any more if the tapering begins. Give me a break, Chris.

Finally, in Paragraphs 16 through 19 of his 29-paragraph report, the AP through Rugaber and Crutsinger got around to relaying a bit of the troubling news in yesterday's jobs brew:

Many of the new jobs are only part time. The number of Americans who said they were working part time but would prefer full-time work jumped 322,000 to 8.2 million - the most in eight months.

That could be a sign that some employers are hiring more part-time workers to avoid the health care reform law's requirement that companies provide health coverage to full-time staff. That mandate was to take effect Jan. 1. But this week, the Obama administration postponed it until 2015.

The rise in part-time jobs helped boost one measure of weakness in the job market - the so-called underemployment rate. This includes not only the unemployed but also people with part-time jobs who want full-time work and people who have stopped looking for work.

In June, the underemployment rate rose from 13.8 percent to 14.3 percent. That's still down from 14.8 percent a year ago. The rate peaked at 17.1 percent in April 2010.

Naturally, I didn't find any mention of the steep decline in full-time employment in any AP report.

Cross-posted at BizzyBlog.com.

{kind=link}